If you follow or own JPM, C, BAC, MS, GS, or European ADRs CS, UBS, DB, you have no doubt observed the relentless stream of negative headlines/announcements underscoring the very challenging operating environment of the global investment banks. In our view these challenges are structural, not cyclical, and we believe that global investment banking model is effectively under siege. In this Insight, we discuss the immense challenges facing the global investment banks and discuss how challenges facing their business model can be directly traced to the role these firms played in the financial crisis. We also address why low returns for the ten to fifteen large global investment banks are likely to persist for several years.

Part #1: Why the Global Investment Banking Model is Under Siege

Part #2: Why the Canadian Investment Banks Largely Avoided the Painful Global Restructuring

Highlights

- Investment Banking Revenues Under Significant Pressure: This most recent earnings season saw a litany of negative headlines/announcements related to the global investment banks, especially for earnings related to fixed income trading. Now, more than six years since the financial crisis, the sector continues to be challenged with many banks making efforts to restructure the global investment banking business model as a whole.

- Investment Banks’ Instability Contributed to Crisis, Making them Regulatory Targets: Traditional, or pre-cycle, measures of credit strength (e.g., Basel Tier 1 ratio) were exposed as inadequate by the credit crisis, as they did not account for the very high levels of financial leverage in the investment banks. This leverage, combined with heavy reliance on short-term funding, created distress in the large and systemically important investment banks, causing financial contagion and accelerating the global crisis. Regulators have responded by targeting the investment banking model, seeking to reduce its potential to exacerbate/cause a future crisis.

- Reduced ROE at Global Investment Banks a Major Consequence of Post-Crisis Regulation: Four main policy changes negatively impacted investment banking profitability. First, stricter/higher liquidity ratios and less reliance on short-term funding, including overnight REPO funding, resulted in lower net interest margins/net interest income. Second, significantly higher required capital levels materially reduced financial leverage, while changes in capital treatments reduced profitability of certain businesses, like bespoke OTC derivatives, reducing ROEs. Third, regulator attempts to delink “speculative” trading from government insured retail deposits through the “Volcker Rule” harmed market making businesses, reduced fixed income trading, one of the largest and most important sources of revenues (also, when combined with large reductions in fixed income trading inventory levels it has contributed to less market liquidity and lower net interest income). And fourth, large fines aimed at “bad actors” weighed on book value/capital growth, while significantly greater regulatory scrutiny has impacted risk appetites. Together, these changes have drastically reduced investment banking ROEs. Up until recently, firms appeared to be hoping that revenues would rebound. However, with little improvements shown since the credit crisis the urgency of these firms to restructure their business model is rising.

- Stock Price Gains Will Be Muted by Low Returns: Regulators succeeded in significantly reducing the risk profile of the global banks/investment banks. However, their resultant policy responses are weighing heavily on returns on capital, and contributing to the ongoing restructuring of the business model, which will take years to complete. In the meantime, low returns are expected to persist for the foreseeable future, weighing on book value growth, multiples, and likely, stock price performance. Although the global investment banks/investment banks have huge market capitalizations and represent ~15% of the global financials index, there are actually less than 20 in total out over well over 1,500 financial services companies worldwide.

Virtually Every Day Brings News of Challenges for the Global Investment Banks

To highlight the challenges the global investment banks are facing, we would note that there is a negative headline regarding these issues almost every day. Below is a sample of headlines from just the past few months:

- JPMorgan (JPM) disclosed a number of negative items at its most recent investor day in February, including: trading revenues down 20% quarter-to-date, investment banking revenues down 25% year-over-year, and large provisioning for oil and gas loans.

- The CEO of Goldman Sachs (GS) highlighted at a recent conference that FICC[1] revenue has declined by US$2.6bln from 2012 to 2015.

- Bank of America (BAC) and Morgan Stanley (MS) announced intentions to reduce expenses related to trading and investment banking, with staff reductions speculated, the latter bank eliminating a quarter of its fixed income trading staff.

- Jefferies, which is now owned by Leucadia (LUK), announced massive declines in its Q1 2016 trading business, in addition to a 15% year-over-year decrease in investment banking revenue[2]. The investment bank reported that trading revenues in fixed income and equities were down 55% and 99%, respectively, from Q1 2015.

- Global investment banks in Europe are not immune from these challenges, as UBS, DB, and CS are all expected to report significantly lower revenue this quarter (UBS recently warned that Q1 investment banking profits could decline 75% year-over-year[3], CS announced that trading revenues were down 40-45%). CS is rumoured to be shopping its U.S. capital markets business.

Everywhere you look, there is evidence that the global investment banking model is under siege.

How did it come to this?

Drawing a Direct Line from Post-Crisis Regulatory Response to Current Challenges

Before the financial crisis, investors measured/assessed capital levels of the global investment banks primarily using their Tier 1 capital ratio (under the Basel regime), with “high” ratios seen as indicative of financial and capital strength (while at the same time, very little attention was given to absolute balance sheet leverage, i.e., assets-to-equity). However, the financial crisis ultimately exposed using only Tier 1 ratios as a measure of capital strength, to the exclusion of absolute leverage, to be a flawed approach, as many global investment banks were able to operate at “high” Basel Tier 1 ratios despite having significant financial leverage. In many instances, these giant firms were able to operate with ratios of assets-to-equity of up to ~50x, because large amounts of their (ultimately troubled) assets were rated “AAA”, and therefore, had low risk-weightings.

When disruption in the fixed income markets emerged in 2008, financial risk from very high leverage/assets-to-equity was exacerbated by the unstable funding models in the independent investment banks, namely high reliance on overnight REPO borrowing (which reduced funding costs, contributing to higher net interest income). This universe of companies included some of the largest investment banks in the world, many with balance sheet sizes in excess of US$1 trillion (i.e., Goldman Sachs, Morgan Stanley, Merrill Lynch, Bear Stearns, and Lehman Brothers). The financial distress that emerged in these huge financial intermediaries served as a source of contagion and a key accelerant to the escalating global credit/financial crisis in 2008/2009.

As a result, the aftermath of the crisis has seen increased regulation targeted at investment banks, as global regulators sought to reduce the probability of a future crisis. Below, we highlight the main policy changes, and identify how they are weighing on current investment bank profitability, specifically, and the business model, generally.

First, regulators sought to strengthen and improve the funding model of the independent investment banks by requiring stricter liquidity ratios, greater use of term funding and lower reliance on overnight funding (the banks also had to significantly increase and extend their sources liquidity). This has resulted in more, and longer duration funding, which has reduced net interest margins and net interest income, a key revenue source.

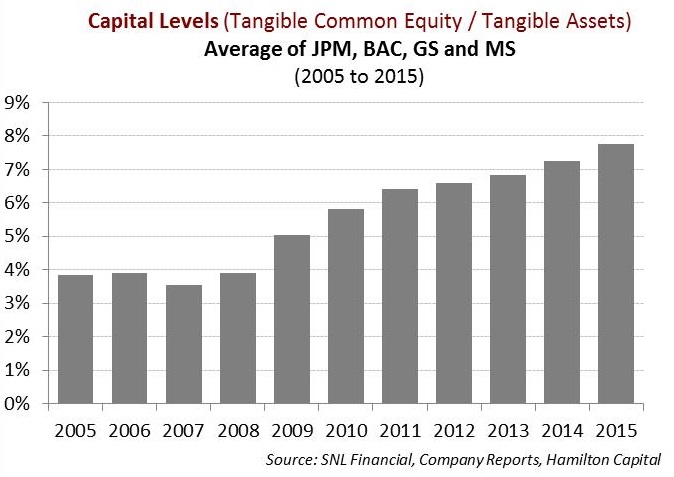

Second, regulators sought to significantly reduce the system’s financial leverage (i.e., assets-to-equity). For the investment banks, this was accomplished in the following ways: (i) raising common equity, (ii) introducing a stricter measurement of risk-weighted assets (including the use of internal models), and (iii) simplifying their business model/exposure to illiquid “Level III” assets (many of which are less relevant to the core financial intermediation between providers and users of capital).

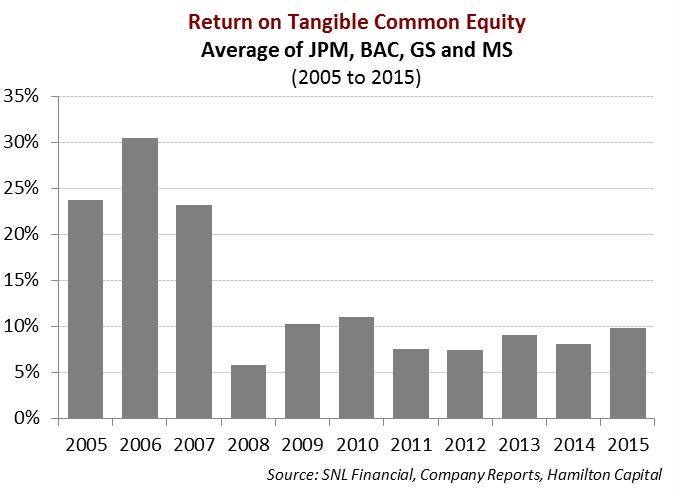

The reduced ROE is evident in certain product lines including bespoke/OTC on-balance sheet derivatives and non-agency mortgage-backed securities (MBS), areas which were formerly large drivers of investment bank profits but are now increasingly challenged businesses due to higher required capital requirements. These capital cushions were made even larger for systemically important financial institutions (SIFIs) and global systemically important financial institutions (G-SIFIs). This had the desired effect of significantly increasing required capital levels, and cutting returns on equity by more than half (see chart below).

Third, regulators sought through the “Volcker Rule” to eliminate any potential intermingling between FDIC government guaranteed retail deposits and institutional speculative, i.e., “proprietary”, trading. This resulted in universal banks that possessed insured retail deposits to be subjected to significant regulatory scrutiny, particularly with respect to market making. Given that the exact point between when legitimate market-making becomes “speculative” trading is not at all clear, this regulatory uncertainty had the effect of reducing market liquidity from the large fixed income trading firms, which has depressed trading revenues, one of the most important revenue sources for global investment banks.

And fourth, regulators sought to “change the culture” of global banking and punish those that they considered “bad actors”. This led to the introduction of significant regulatory imposed fines for a number of activities, including: LIBOR fixing, FX manipulation, and residential MBS (RMBS) misrepresentations. The resultant fines have been in the tens of billions of dollars, further weighing on capital ratios and ultimately ROE.

Summary: A Sector Struggling to Raise Returns on Capital

Together, these changes have resulted in large declines in return on equity for the investment banks, necessitating attempts to restructure their business models to generate returns higher than their cost of capital (in the low to mid-teens as a percentage of equity). The current weak market environment is adding to these challenges by weighing on stock prices and investor sentiment. Unfortunately, we see the global independent investment banks continuing to experience significant challenges, and given their sheer size, continuing to negatively impact investor sentiment.

In the years immediately following the credit crisis, the sector has attempted to increase ROEs through the following: (i) reduce compensation cash ratios, (ii) deferring compensation by adding more stock-based compensation, and (iii) reducing exposures to high capital density assets. It also appeared as if management teams believed that revenues/volumes would ultimately rebound, or normalize at materially higher levels, which combined with steps taken would take ROEs into the mid-teens.

This of course, has not happened as revenues never rebounded, keeping ROEs stubbornly close to, or even below the cost of capital. As a result, the sector is now moving to the point where it will need to restructure its business model to operate in a lower revenues environment. This will ultimately result in the repricing of multiple products and put further pressure on expenses, especially compensation.

In our view, the restructuring of the business model will take years.

In the meantime, we expect these low returns to persist, which will weigh on share price performance, potentially limiting share prices to growth in book values. That being said, although the global investment banks dominate headlines and represent a large weighting in the global financial sector universe, at ~15% of the S&P Global 1200 Financial Sector Index, they are but a relatively small number of companies.

This Insight should be read in conjunction with our Notes from NYC: For Global Investment Banks, Legacy Issues and Volatile Markets Creating Challenges (23/03/16), in which we discuss the findings from our meetings with 7 banks, including 6 international banks.

Notes

[1] FICC is the abbreviation for Fixed Income, Currencies and Commodities trading.

[2] Jefferies Q1 2016 ended on February 29, 2016.

[3] Source: Barclays.